Bandar Abbas, April 2026. The tanker captain knows this route well. He has sailed it a hundred times — through the Strait of Hormuz, into the Gulf of Oman, west toward the refineries. This month, he cannot sail it at all. Conflict has choked the world’s most important oil corridor. Roughly nine million barrels per day, nearly a tenth of global supply, disappeared almost overnight.

In earlier decades, a disruption like this would have been painful but manageable. Strategic reserves, spare production capacity, and diversified supply chains would have softened the blow. This time, Brent crude surged above $100 per barrel, diesel approached $6 per gallon, and inventories fell below their five-year average. The cushion was gone.

What happened in the Strait of Hormuz is not terribly unusual. Geopolitical shocks to supply are as old as oil markets themselves. But why, this time, did the global energy system have so little capacity left to absorb one? The answer lies not in the Persian Gulf, but in two decades of policy that steadily dismantled the capital structure of the fuels the world still depends on, while simultaneously obstructing the only scalable alternative capable of replacing them.

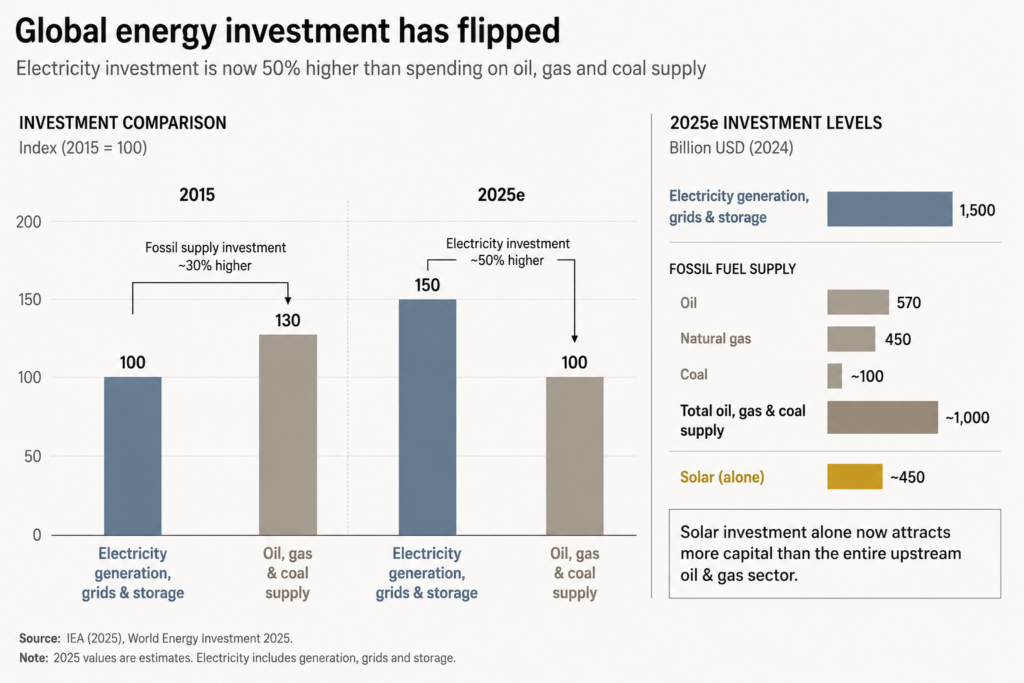

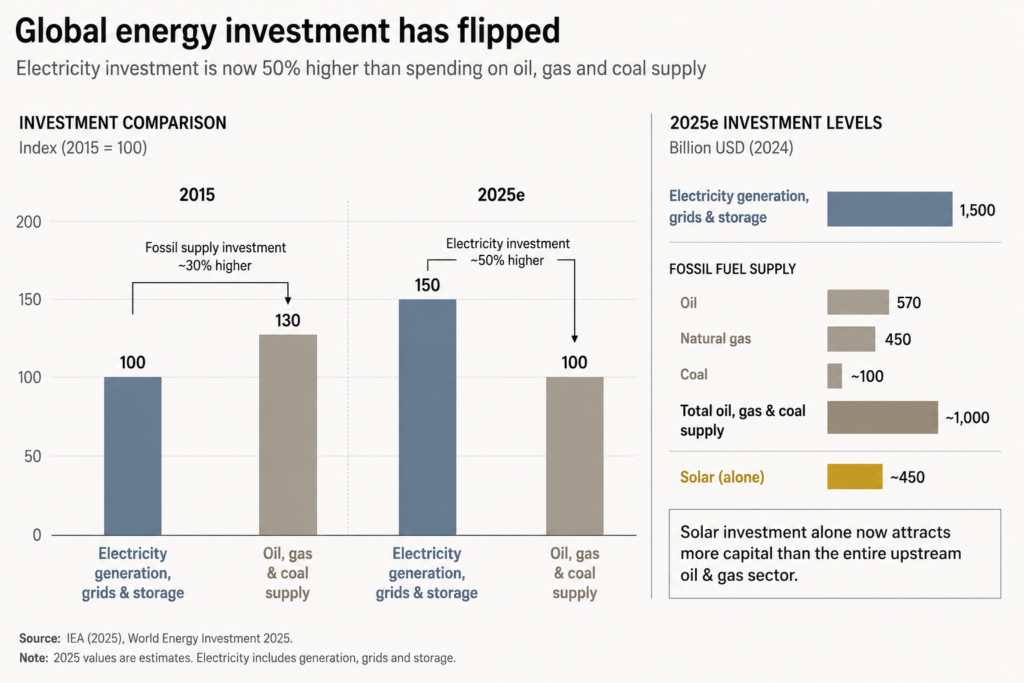

The International Energy Agency’s investment data clearly tells the story. A decade ago, fossil fuel investment exceeded spending on electricity generation, grids, and storage by roughly 30 percent. By 2025, the relationship had completely reversed. Electricity investment now runs roughly 50 percent above the combined total for oil, natural gas, and coal. Solar investment alone attracts more capital annually than the entire upstream oil and gas sector.

This shift did not occur because markets concluded fossil fuels were no longer necessary. It occurred because governments decided they should become less important. Subsidies, mandates, ESG pressure on institutional lenders, and regulatory hostility toward new fossil fuel infrastructure all pushed capital in the same direction.

Imagine a farmer told he may only plant one crop in the future — a promising new variety, but one not yet tested in every season or climate. At the same time, the grain silos storing the old harvest are quietly dismantled. If the new crop performs perfectly, the transition succeeds. But if the harvest disappoints, or arrives late, or fails during a drought, there is nowhere left to turn. The silos are gone. That precarity reflects the position of the modern energy system.

When governments distort the price signals that coordinate investment in capital-intensive industries, capital flows somewhere other than where it is most urgently needed. The consequences do not appear immediately. They accumulate slowly, in the form of deferred maintenance, abandoned projects, shrinking spare capacity, and reduced resilience. The system appears stable until a shock arrives that it can no longer absorb.

The IEA reports that nearly 90 percent of upstream oil and gas investment since 2019 has gone not toward expanding production but merely toward offsetting natural field decline. The industry is running faster to stand still, and doing so with a shrinking capital base. The supply pipeline for the late 2020s is being shaped right now, and the investment decisions of 2020 and 2021 have already made it thinner than the world can comfortably afford.

Exactly one technology is capable of generating reliable, large-scale, zero-carbon electricity regardless of weather, season, or time of day. It is not solar. It is not wind. Both are intermittent by nature. The technology is nuclear power, and the same regulatory culture that pushed fossil fuels out of the energy mix spent decades ensuring nuclear power could not replace them.

Between 1954 and 1978, the United States authorized the construction of 133 nuclear reactors. Since 1978, only two have entered commercial operation. The permitting and construction timeline for a new nuclear facility now frequently exceeds twenty years. Regulatory costs alone can reach tens of millions of dollars annually before a single kilowatt-hour is generated.

Nuclear power did not become uneconomic because consumers stopped wanting reliable electricity. It became uneconomic because regulators made it so — layer by layer, decade by decade, requirement by requirement — until the economics no longer worked. The same political impulse that declared fossil fuels incompatible with a sustainable future also prevented its only scalable replacement from being built on the necessary timeline and budget.

One critical miscalculation is at the centre of the present crisis: activists planned to move away from fossil fuels without ensuring a destination existed first. Part of the old capital structure was dismantled before the replacement was ready. In the gap between the two, the system’s resilience quietly disappeared.

Into this increasingly fragile system has arrived a demand shock few policymakers anticipated. Artificial intelligence and data centers are driving the fastest growth in global electricity demand in more than a decade. Large data centers consume as much electricity as small cities do, continuously and without interruption. This is precisely the kind of demand profile that reliable baseload generation was designed to meet — and precisely the kind that intermittent renewables cannot reliably satisfy alone.

It might sound like a degrowth conspiracy, but it’s simply structural pressure. Suppressing reliable baseload investment created a system with steadily shrinking resilience. The AI-driven surge in demand merely exposed the weakness. Had fossil fuel investment been allowed to follow market price signals toward market-supported expansion, and had nuclear power remained economically viable to construct, the system would likely have retained enough margin to absorb both rising demand and geopolitical disruption. Instead, the margin disappeared.

Grid infrastructure tells a similar story. Investment in transmission networks has lagged far behind investment in generation capacity. The infrastructure needed to connect newly generated supply to new areas of demand remains trapped inside the same permitting bottlenecks that crippled nuclear development. The same regulatory instinct that created the fragility is now obstructing market attempts to repair it.

Ludwig von Mises identified the central logic of interventionism long ago: one intervention creates distortions that appear to require additional interventions to correct, until the system itself becomes dependent on political management rather than economic coordination. The modern energy system has drifted deep into that logic. Fossil fuel investment was redirected politically. The resulting fragility was temporarily hidden by weak demand growth. Nuclear power, the natural corrective, was regulated into stagnation. The AI-driven surge in electricity removed the remaining slack. Then a geopolitical shock in the Strait of Hormuz exposed what years of distorted investment signals had quietly created.

Every barrel of oil above $100 is the energy system presenting the invoice for years of suppressed price signals and redirected capital allocation. The hundreds of billions of dollars in upstream investment that never materialized do not vanish harmlessly. They return later as supply shortages, higher prices, and reduced resilience — precisely when geopolitical instability removes the last remaining buffer.

A genuinely market-driven energy system would not have produced perfection. But it likely would have produced resilience. Absent intervention, price signals encourage additional baseload investment before shortages become acute. Capital flows toward nuclear generation before regulatory costs make construction prohibitively slow and expensive. The energy transition would have proceeded at the pace the underlying capital structure could realistically support.

The tanker captain still cannot sail his route. Consumers see the consequences in every electricity bill and every trip to the gas station. These are not merely the costs of a geopolitical crisis. They are the delayed costs of the policies that made the energy system unable to withstand one.