Jerome Powell’s term as Federal Reserve chair ended Friday, and assessments of his legacy are already rolling in.

At Bloomberg, Amara Omeokwe and Catarina Saraiva describe Powell as “The Fed Chair Who Fought Back.” At Forbes, Danielle Chemtobe says he “leaves behind a legacy of navigating inflation and defending the independence of the central bank under pressure from the president of the United States.” Greg Robb, at MarketWatch, says “Powell’s legacy as Fed chair is fighting inflation and Trump.” Jamie McGeever, at Reuters, describes him as the “Defender-in-Chief.” Squawk on the Street’s Sara Eisen recounts Powell’s legacy as “a champion for Fed independence, saving the world economy from a deep depression during the COVID shutdown, and fighting 41-year high inflation without wrecking the economy or jobs, achieving the rare soft landing.”

If these early accounts hold up, Powell will be remembered as a fighter — and a successful fighter, at that. He is widely believed to have protected the economy in the pandemic and shielded the Fed from political pressure. But his record, on both counts, is somewhat mixed.

Powell and the Pandemic

When the economy contracted in early 2020, Powell vowed to do whatever it would take to facilitate a speedy recovery. The Fed, under his leadership, moved quickly to increase the monetary base, cut the interest rate it paid on reserves, and open a host of emergency lending facilities. The Fed’s efforts, Powell told the Senate Banking Committee in May 2020, were intended “to facilitate more directly the flow of credit to households, businesses, and state and local governments” to prevent them from failing during the pandemic.

At least in hindsight, however, Powell’s Fed appears to have done too much.

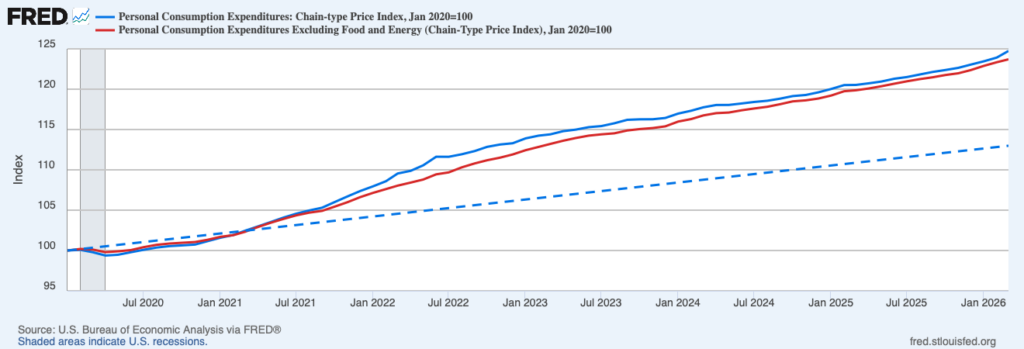

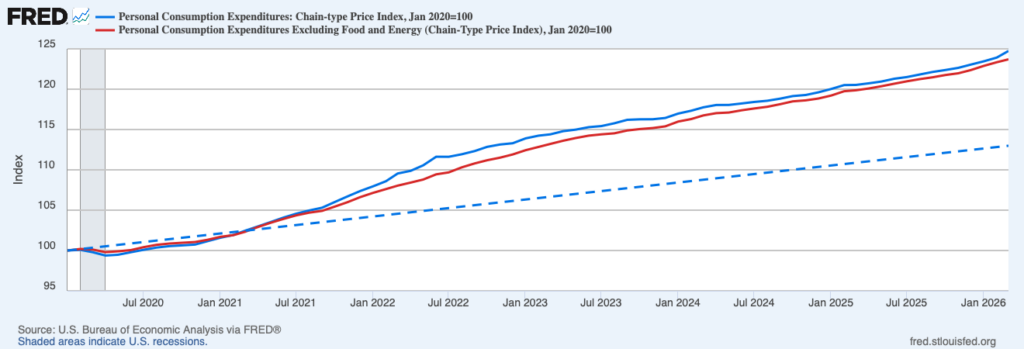

As the economy reopened and real output recovered, the additional liquidity pushed prices higher. The Personal Consumption Expenditures Price Index, which is the Fed’s preferred measure of inflation, grew 13.9 percent from January 2020 to January 2023 — or, roughly 4.3 percent per year. The excess inflation left prices around 7.8 percent higher than they would have been had the Fed hit its two-percent inflation target over the period. The recovery was speedy. But the cost was higher inflation.

No doubt some will try to absolve Powell of the high inflation in 2021 and 2022. Many initially attributed the higher prices to pandemic-related supply disruptions and, later, Russia’s invasion of Ukraine. And some still believe constrained supplies — not Fed policy — are largely to blame.

As I explained at the time, however, temporary supply disruptions cannot account for the permanent rise in prices:

Temporary supply disturbances are temporary. The pandemic and corresponding restrictions reduced our ability to produce. But they will not reduce our ability to produce forever. The lifting of restrictions, vaccine rollout, and gradual acceptance that a mild version of the virus is endemic will eventually permit production to return to normal, even if it has not done so already. […] When production returns to normal, so too do prices. But that is not what the Fed is projecting. Instead, the Fed is projecting that prices will remain permanently elevated. Why would a temporary supply disturbance cause a permanent increase in the level of prices?

Production had mostly returned to its pre-pandemic growth path by 2021:Q3. But prices remained elevated. Indeed, they were growing more rapidly. The implication, as I said then and would repeat in the months that followed, was clear: much of the inflation — and certainly the lasting component — was demand-driven.

Although Powell initially thought inflation was supply-driven, he eventually came to accept that there was a demand-side problem, as well. He famously abandoned the term “transitory” in November 2021. And, as Bill Bergman and I have shown, the Federal Open Market Committee (FOMC) revised its statement in December 2021 to acknowledge “Supply and demand imbalances […] continued to contribute to elevated levels of inflation” (emphasis added). I think Powell — and others at the FOMC — should have recognized the demand-side problem by September 2021. But he did ultimately recognize it.

One might give Powell a pass for only belatedly seeing the demand-side problem and the corresponding need to tighten monetary policy. But should he get credit for bringing down inflation once the problem was understood?

Powell seems to think so. “We looked at the inflation as transitory,” he told journalists in January 2025. “And when the data turned against that in late [20]21, we changed our view, and we raised rates a lot. And here we are at 4.1 percent unemployment and inflation way down.” The Fed, in Powell’s telling, acted “quite vigorously […] once we decided that that’s what we should do.”

In fact, the Powell Fed was rather slow to tighten monetary policy even after it realized there was a demand-side problem.

Bryan Cutsinger and I have described the policy response:

Although the FOMC clearly acknowledged the increase in aggregate demand by December 2021, it did not immediately raise its policy rate. Instead, the FOMC began tapering its asset purchases and indicated it would likely begin raising its policy rate in March 2022. According to the December 2021 Summary of Economic Projections, the median FOMC member thought the midpoint of the federal funds rate would rise to 0.9 percent in 2022, consistent with a 0.75 to 1.0 percent target range.

[…]

To make matters worse, the FOMC was slow to revise the pace of its policy rate hikes once it realized the problem was much worse than it had previously thought. And it realized the problem was much worse pretty quickly.

The FOMC would begin raising its federal funds rate target in March 2022, as it had indicated it would. But the real federal funds rate remained negative through June 2022. “The Fed had eased off the accelerator,” we write, “but had not yet hit the brakes.”

Why didn’t the FOMC raise rates at its December 2021 or January 2022 meetings? Why did it only raise rates by 25 basis points in March? Why did it leave real rates negative through June 2022? Under Powell’s leadership, the FOMC was not merely late to recognize the demand-side problem. It was also slow to tighten monetary policy once the problem was realized.

Indeed, it is still trying to get inflation back down to 2 percent. Powell cites a “series of shocks,” including President Trump’s tariffs and the more recent conflict in the Middle East, for the lack of progress. But the problem now, as in late 2021, is excess nominal spending growth.

Powell and Political Pressure

Whereas some assessments of Powell’s legacy acknowledge his mixed record on inflation, the claim that he is a champion of central bank independence usually goes unchallenged. In March 2026, the American Society for Public Administration awarded him the Paul A. Volcker Public Integrity Award for “upholding a standard of faithful service impermeable to political pressure.” But here, too, Powell’s record is mixed: he allowed the Fed to drift into politically-charged areas and appears to have yielded to political pressure from the Biden administration.

Until very recently, Powell appears to have done little to abate the Fed’s mission creep into social justice topics. Louis Rouanet and Alex Salter document the “growing interest by Fed officials in ‘social justice’ topics, as opposed to topics strictly related to the goals set forth by Congress,” in the years just prior to the pandemic. Then, in 2020, the Fed revised its Statement on Longer-Run Goals and Monetary Policy Strategy to describe its employment objective as a “broad-based and inclusive goal,” which seemed to suggest the Fed was considering racial employment gaps. “While such gaps clearly exist,” Rouanet and Salter write,

they are structural: They persist regardless of short-run aggregate demand fluctuations. This means the Fed has adopted a goal that it cannot achieve without further embracing direct resource allocation, which is de facto fiscal policy, at the expense of liquidity provision. It also pulls the Fed further into the political arena by making central bankers allocators of scarce resources according to political, and perhaps partisan, criteria. Such actions are, at minimum, in tension with democratic governance.

The Fed dropped the phrase from its 2025 revision, despite Powell having explicitly affirmed it in prior years.

Powell also permitted the Fed to drift into climate policy. The Fed joined the Network of Central Banks and Supervisors for Greening the Financial System in 2020 and began pressuring banks to disclose climate risks and develop regulatory tools for climate stress testing thereafter. In 2023, Powell said the Fed has “narrow, but important, responsibilities regarding climate-related financial risks” and that the “public reasonably expects supervisors to require that banks understand, and appropriately manage, their material risks, including the financial risks of climate change.” The Fed withdrew from the Network of Central Banks and Supervisors for Greening the Financial System in 2025 — just three days before President Trump’s inauguration.

Regardless of what one thinks about social justice or climate policy, these topics clearly fall beyond the Fed’s mandate. Allowing the Fed to dabble in these politically-charged areas did not bolster its independence. It eroded it. And, although the Fed has since stepped back in both areas under Powell’s leadership, the damage to its independence has already been done.

Some have also claimed political factors are responsible for the delayed response to rising inflation in late 2021 and early 2022, as Gregg Robb reports:

Billionaire macro-trading legend Paul Tudor Jones suggested that Powell held off on raising interest rates — which were stuck close to zero for all of 2021 — because he wanted then-President Joe Biden to reappoint him. Biden was hoping a strong economy fueled by lower rates would help him get re-elected.

After Biden nominated Powell for a second term, ‘it was go time’ for rate hikes, Jones said in a podcast interview last month.

The timing is certainly curious. The Fed clearly acknowledged the demand-side problem in December 2021. But it did not raise its federal funds rate target until March 2022, and only by 25 basis points then. When the Fed raised its target by 50 basis points in May 2022, Powell said “a 75-basis-point increase is not something the Committee is actively considering.” Then he was confirmed and the tenor changed. The Fed raised its federal funds rate target by 75 basis points at each of the four meetings that followed Powell’s confirmation.

Further evidence that Powell relented to political pressure under the Biden administration comes from his visit to the White House in May 2022. While it is not unusual for a Fed chair to visit the White House, the meetings typically take place behind closed doors. They do not usually involve a press gaggle in the Oval Office. Many viewed the event as an opportunity for the president to “deflect blame back to the Fed” or “passing the buck” to the Fed chair ahead of the election, and Powell appeared to serve as a willing political tool.

Inflation, Independence, and Powell’s Legacy

There is no denying the difficulties the Fed has faced under Powell’s leadership, and he deserves credit for building consensus and instilling confidence in uncertain times. He has a remarkably cool demeanor and has managed to keep his cool despite ongoing pressure from politicians on both sides of the aisle. But one should not let affection for Powell — or, disaffection for President Trump — cloud one’s judgment.

A sober assessment of the actual decisions made and outcomes realized reveals a mixed record for Powell. His legacy is not great, but it could have been much worse.